Spotlight on Prevented Losses

Most FWA programs rely on recoveries and savings as the measure of success. But there is another critical component that's a hidden risk and amounts to big dollars: Prevented Losses. We are bringing prevented losses to the forefront, not just in concept, but also in terms of the financial impact on healthcare payment integrity. This article discusses challenges that continue to exist and what we need to do as an industry in order to continue to evolve the value of our FWA programs.

Spotlight: A Fundamental Shift in Capturing FWA Prevention Efforts

The Most Significant Metric that Impacts the Healthcare Industry

Introduction

You may not like what you are about to read. In fact, this may be a wildly unpopular point of view – we’re here to tell you that if you’re in the fight to prevent healthcare fraud, waste and abuse and you are not actively looking for or capturing prevented losses – you are missing out on one of the best ways to demonstrate the value of FWA efforts to your organization and to our industry. This includes everyone – healthcare payers, state and federal regulators, vendors, legislators – everyone.

We are not suggesting we stop pursuing recoveries or savings. If you are thinking ‘savings are prevented losses, aren’t they?’ well, in some ways, you’re right. Many have used savings and prevented loss interchangeably. To be completely fair, there is overlap between what is considered savings versus prevented loss as we will dive into shortly. The challenge and differentiation among them is in how we quantify it. The prevented losses we want to talk about today are the hard to quantify kind that most teams are usually not capturing or reporting and, when combined with savings and prevented losses, really make up the sphere of healthcare payment integrity.

The purpose of this article is to explain why we believe prevented losses should be your new best friend and why our industry needs to change the way we look at FWA by placing more emphasis on the valuable efforts taken by FWA teams across the country. Although we don’t have clear answers about how to solve this particular challenge, we do believe it’s a problem worth solving if you fight healthcare fraud, waste and abuse. After you read this, you may have more questions than you started with and that’s ok. As long as you are thinking about it, we’re moving in the right direction. To figure out where we're going, we need to look at where we started to understand how we got here in the first place.

F Comes Before W.

There’s a reason the F comes first in “FWA.” Before there was so much attention on waste – there was fraud and abuse. Enforcement efforts focused on prosecution and restitution, a form of recovery which requires the defendant to pay back the monies gained through fraudulent and abusive behavior.

That set the tone for our industry. With the increased awareness of health plan SIU’s - we looked for ways to ‘get the bad guys’ and most of the technology available looked at paid claims. Cases were built on the amounts paid for alleged fraudulent or improper billing behavior. In the 90’s, there weren’t as many headlines with the word “millions” in them, let alone “billions.”

Clearly, times have changed. But who could have known how much healthcare spend would grow and how significant our challenge would be with that change?

With additional enhancements and capabilities, some became more comfortable with shifting from the age-old pay and chase to prepayment denials of claims (savings). Of course, there were claims edit systems that caught a lot, but there was also a lot that wasn’t caught. Although most of our investigations were still initiated after claims were paid, we realized preventing some of the bad payments was pretty important too.

Today, most organizations are still focused on recoveries, some are focused on prepayment denials and few plans are looking at prevented losses. We have a ton of work to do; we are strapped for additional resources and time.

All while healthcare spend grows more each year and our ability to curtail the losses doesn’t keep up.

What are Prevented Losses?

If you are in the payment integrity industry, then you know about recoveries and savings related to improper payments. They tend to be the two main areas of focus when we talk about return on investment (ROI) related to FWA efforts. But what we’ve learned over the years is that prevented losses are, dare we say, MORE important than savings and recoveries. You may completely disagree with this notion, and that’s ok... let’s discuss.

Recoveries and savings require a claim being submitted for payment. You either pay the claim and have to chase the recovery OR you stop the claim from being paid (hence the savings). In either instance, you have a claim submission that can be identified, tracked and quantified.

Prevented loss is the impact to an organization related to some benefit that was achieved by the implementation of a process improvement or a change in provider behavior initiated by the FWA team or SIU. Sometimes this can be quantified somewhat easily, other times it’s not so easy. These amounts are not associated with a specific claim submission, because you are trying to prevent an improper claim from being submitted in the first place. So, you don’t have an actual claim that you can track and quantify. But this is precisely why it’s such a valuable measure.

Prevented losses are critical in that they capture the benefit of all the work your team puts in, not just to investigate cases, but also the ways the FWA team contributes to the overall organization and industry as a whole. Essentially, identifying and quantifying prevented losses should be the main reason for our existence. Yes, we’ve been historically trained to look for higher recoveries and savings. But when comparing prevented losses to savings and recoveries, prevented loss has the potential to provide better long-term impact to healthcare and is less administratively burdensome to execute. It also just happens to be the hardest to quantify.

When you identify an issue that can save money from being inappropriately paid for the foreseeable future – don’t you think that might be something worth talking about? We do. So does the Department of Justice (DOJ) and the Centers for Medicaid and MedicareServices (CMS). But first, let’s start with the definition published in 2007 when NHCAA convened a workgroup to help define the most common terms used in our industry, including Prevented Loss.

2007 ROI Definitions Guidance for Prevented Loss

(Printed with Permission from NHCAA)

Objective: To define those reportable amounts associated with losses prevented on a pre-payment basis where an actual claim was not submitted as a result of SIU activity.

Definition: A quantifiable financial impact resulting from the direct action(s) initiated and completed by the SIU. The quantifiable impact may be the result of:

a. Change in Behavior—External, Claims Related

b. Process Improvement—Internal Impact

a. Change in Behavior - A clear change in the billing pattern with a direct relationship to SIU actions, the result of which is a quantifiable financial impact. This impact must be measured “real time”, and not projected, or forecasted into the future. The change in behavior measurement is recorded for the lesser of the length of the scheme, or 12 months from the resolution of the issue with the provider.

b. Process Improvement - A specific and quantifiable financial impact resulting from the modification of internal policy, edit or process. These changes must be the direct result of actions taken or recommendations made by the SIU. The measured results are limited to 12 months.

GUIDANCE

Key points to consider about this definition include:

Quantifiable Financial Impact: Quantifiable financial impact shall mean that through a documented system of measurement, you will clearly be able to demonstrate that a beneficial impact was achieved by reducing the suspect behavior, and as such, the overall payments.

Real Time: Real time shall mean that the impact is measured at regular intervals, most often monthly. No forecasts, or assumptions shall be made. For example, impact through January will be measured once January has closed, and January claim receipts are able to be reported against.

One special note related to timing. As impact will be measured “real time” should the measurement cross years, it is conceivable that the 12-month period will include some measures from both a current, and previous year.

Direct Relationship to SIU: Direct relationship to the SIU shall mean that the SIU must be the driver behind the discovery, review and recommendations made. Recommendations resulting from consultants, vendors, or other departments shall not be included in this category, except in those cases when such a subject matter expert is engaged by the SIU for the specific purpose of reviewing and making recommendations relative to an issue identified by the SIU.

The SIU is not obligated to write or program any related policy or edit, but must be the driver behind the identification, quantification and recommendations that compel such change.

We Told You We Aren’t the Only Ones Who Think It’s a Big Deal!

The government has recognized the importance of prevented losses - well beyond 12 months. In 2014, CMS reported outcomes of the Fraud Prevention System (FPS) and noted projected savings or avoidance – essentially prevented losses.

“The true financial impact of the FPS, however, is much harder to measure: once CMS uses the information from an FPS lead to impose a money-stopping administrative action against a crooked provider (such as revoking billing privileges), the benefit to the U.S taxpayer is not limited to monies recovered, but includes any future billings by that provider which were prevented. These kinds of future costs avoided are difficult to estimate with certainty, and for this reason have not been – until now – systematically measured or audited in either the public or private sectors.”

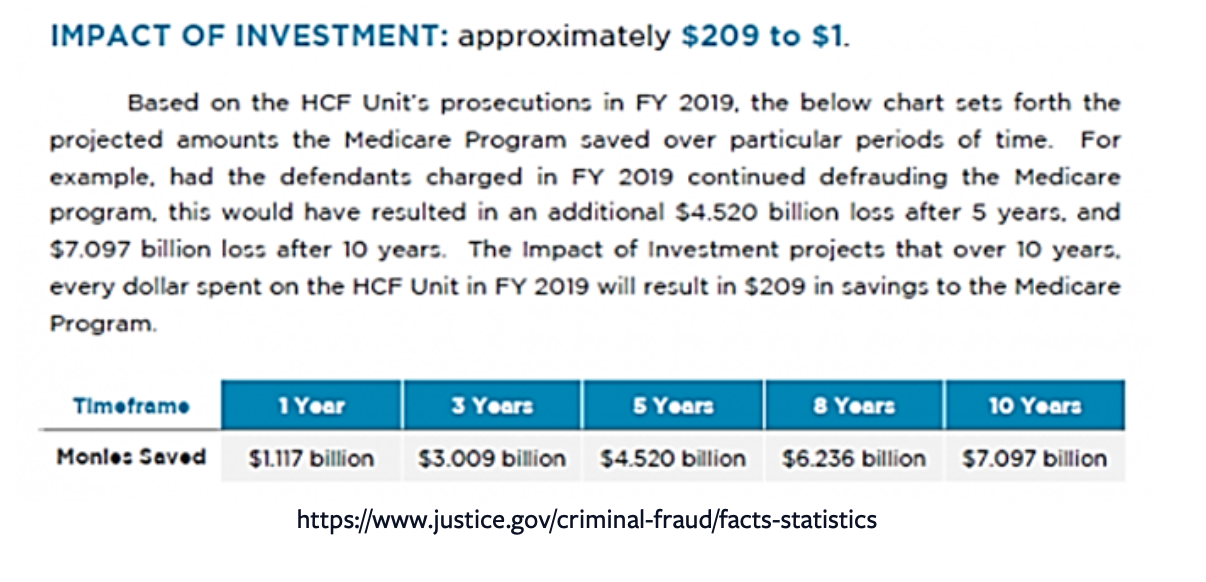

Even the Department of Justice highlights the following projected savings to the Medicare Program.

If CMS and DOJ acknowledge the long-term value in prevented loss, shouldn’t we?

Let’s reevaluate our industry standards.

A Shift in the Industry Mindset is Imperative.

If asked, most FWA teams would tell you that they do not think their contribution is adequately represented by savings and recoveries alone. Their efforts and impact expand far beyond those two numbers. But there are plenty of reasons why prevented losses don’t get as much attention:

It's Just Harder to Quantify.

This is probably the number one reason why many organizations are not ready to talk about it yet. Without an easy formula, the worry of misstating is real, so many just avoid it.

Conflicting Priorities.

Prevented loss initiatives may conflict with the goals of other business units. For example, network adequacy needs may trump the ability to terminate a provider from a managed care organization (MCO) network.

Prepay for Perpetuity.

It’s much easier to leave a provider on prepay and stop any claims that might get paid inappropriately, capturing savings, one of the important components of ROI. Plus, there is no guidance about how long you should keep a provider on prepay.

Regulatory Requirements.

Many regulatory reporting and referral criteria focus primarily on paid amounts. For example, when we make referrals to regulatory agencies and law enforcement, they are generally focused on the merits of the case related to dollars spent and patient risk. Whereas annual reporting focuses on recoveries, followed by savings, and to a much lesser degree, prevented losses.

Recovery and Savings Goals Prevail.

Many payers still view recoveries and savings as the most important measure of an SIU’s performance. When the team is viewed as a revenue generating part of the organization, it’s hard to change that.

Justification for Bodies.

It’s way easier to justify staffing when you can point to a growing case backlog that leads to hard dollar recoveries and savings. It's much harder to get buy-in if you lead with "I'd like to hire someone to help find prevented losses."

Having said all that – we cannot get away from the fact that identifying and preventing improper claim submissions is far more valuable than recoveries and savings because it also results in other improvements to the ‘system’ – whether it be your internal plan or the healthcare system as a whole. It captures benefits that are a part of our day-to-day such as provider education, risk identification, the integrity of the provider network, edit and policy recommendations, improvement of process inefficiencies and so much more.

It makes an impact on improving healthcare payment integrity, which, in turn, promotes everything that our healthcare programs hope to achieve - from lowering the cost of healthcare to improving the quality of care provided to patients. Prevented losses are one of the biggest steps we can take to making an impact on the US healthcare system.

How Do You Quantify It?

Although NHCAA provided guidance about how to quantity prevented losses in 2007, this is still an area that most struggle with, and we believe the consistency of the methodology across our industry is part of the reason why the impact is so understated. Even state and Federal regulators do not all have a consistent calculation, although some have adopted similar language to what NHCAA published.

Following NHCAA guidance, for those events that can be quantified, means finding a specific event found / initiated by SIU that changed a behavior or process. Whether it be provider education, policy implementation, or process change - that is the point from which you should look backwards 12 months and forward 12 months. Looking back allows you to see what the spend looked like before the change. Looking forward allows you to identify what the spend would be if you did nothing. And just like any metric, you must be able to refer back to the data used to justify numbers that you report.

Here are some simple examples where prevented losses might be more easily quantified than others:

Change in Behavior.

Upcoding. Provider is billing all 99215 E&Ms. SIU educates the provider and he begins to shift billing to 99213 and 99214 as appropriate. SIU captures the difference paid from the past 12 months (99215) to the more appropriate billing of 99213 and 99214 and capture the prevented loss 12 months forward.

Process Improvement.

Pre-authorization Review. Some health plans involve their SIU clinical staff in the pre-authorization process for areas that are more ripe for FWA (e.g., genetic testing). If the transition to SIU clinical staff conducting these reviews results in less authorizations, capture these amounts as prevented losses. We don’t have a claim submission (so it's not a savings), but we do have the auth for services that can be used to quantify.

Unfortunately, not all scenarios are as cut and dry.

Credentialing – The FWA team provided training to members of the credentialing unit and described what to look for during the provider credentialing process that might go undetected. As a result, they credentialed 10% less providers than the prior year. We don’t know how much those providers would have billed us if they would have been credentialed instead. How do we quantify that?

Policy implementation - Due to an SIU initiative, the plan instituted a limit on the number of units covered. Providers were submitting 10 units for the first year but the plan only paid 4 units and denied the other six. Do we get to count the 6 we denied for a year as prevented loss or is it a savings? We would argue the 6 units that were actually submitted as claims should be considered savings, but if the claim submissions decreased, that should be captured as prevented loss, due to the change in behavior. Some organizations might capture it all as savings.

What You Can Do.

Prevented losses equate to risk. If you start to shift attention to this, it may make many people uncomfortable. Identifying risk tends to insinuate that someone dropped the ball or didn’t do their job. But that’s not the case.

The first piece of advice we provide our clients is to start the conversation. Whether you are part of a workgroup or not, you can begin initiating and inviting conversations. More mature programs regularly identify opportunities that impact the organization at an enterprise level.

Track. Document. Discuss.

Track initiatives that impact the organization and historical behavior that helps project the benefits of initiatives moving forward.

Document your prevented loss methodology. Even if it is the same as what the NHCAA published, document it in your standard processes.

Discuss internally and externally:

Talk to leadership and describe the value to your organization. Reach out to other teams within your organization to coordinate efforts. Working with your enrollment, medical management, vendor management or actuarial team may help identify systemic risks to the company that lead to prevented losses.

Work with your vendors, industry peers and consultants to determine prevented loss opportunities within your organization. Examine whether your vendors are incentivized to help you prevent losses long term.

On the Horizon.

Jala recently spoke with Lou Saccoccio, CEO of NHCAA, about how prevented losses are being highlighted at health plans. Lou shared that the NHCAA Board of Directors is reexamining the prevented loss definitions to see what advances have been made in the last 14 years within the SIU with respect to preventing fraud losses to see if they should be expanded or revised. We are hopeful that the effort leads to further recognition of the value of prevented losses.

Conclusion.

In order for our industry, as a whole, to accept prevented losses as a dominant measure of FWA prevention efforts, a lot has to change. Perceptions, expectations and approaches are just the start. We don’t know exactly how we will change it, but it’s not out of reach. We can think of a few things that can help us get there:

Payers must support the SIU's putting more effort into identifying broader impacts beyond retroactive identification, chasing recoveries and prepayment claims monitoring.

State and Federal regulatory agencies should shift more focus from recoveries and savings associated with fraud allegations to highlighting how prevention efforts curb losses.

Vendors should be incentivized to help improve payment integrity by assisting in the identification and mitigation of risks to the organization. A good business partner will agree, and will create a mutually beneficial payment structure.

Most people in the healthcare payment integrity industry don’t start their career thinking, “I’m going to help improve healthcare.” But what if we did? We learned the ropes, worked cases and did our jobs the best we could... but were we really focused on improvement of the whole system Or was it just our cases? Because after so long being in this industry, many of us feel more strongly than ever that there needs to be a shift in the FWA prevention mindset.

Shining a spotlight on prevented losses is not only the right path, but it’s also the natural evolution of our industry if we are going to make an impact on overall healthcare payment integrity. We are asking all of you in the industry to invite the conversation. Socialize the concept of the true impact of doing what’s right in preventing FWA - not just what’s been acceptable in the past because it’s easier. Get uncomfortable with us.

“In any given moment we have two options: To step forward into growth or to step back into safety.”

If you have feedback we'd love to hear it. If you have questions and are interested in a 60 minute call to pick our brain, book a complimentary hour with us.

Integrity Advantage is the way healthcare payers reimagine the value of their fraud, waste and abuse program.

We provide FWA services to payers around the country. If you need a program assessment, program growth strategy, investigations, medical reviews or training support -- reach out today.

We are a certified Women’s Business Enterprise (WBE) and an Economically Disadvantaged Woman Owned Small Business (EDWOSB).

For more information click below, call us at 866-644-7799 or email info@integrityadvantage.com.